Complete Financial Tracker Part 1

Want to see the Tracker in full force? Lets look at my end-of-month tracker and the information embedded within. Part 2 coming Feb 15th!

Complete Financial Tracker Part 1

In this edition of The Personal Finance Project Newsletter:

Context - the story told by my August Tracker.

Tracking Debt and Taxes.

“Fun” Spending - let the good times roll!

Prerequisites

October 1st, 2022 - Intro to Financial Tracking

Context

Growing from last week’s Substack on How to Begin Financial Tracking, I thought that showing you a completed tracker may tie things together nicely.

Over the next two Substacks, we will take a journey through my August 2022 tracker. We will stop to chat about the interesting components and additions, which should guide you in tracking your finances.

I must disclose:

I edited some transactions for the sake of privacy, but an honest look at my finances is still the foundation.

The actual template I use is slightly different than this one, so I had to make some edits to fit my tracker in here. (Perhaps in the future I will drop my actual tracker - for those who are looking for some more power).

I have hidden column F in the ledger, which I used to calculate the dollar equivalent of my euro spending. You’ll see in some ledger amounts the expression ‘[@[EX Multiple]]’. Ignore it unless you’re curious.

And most importantly…

None of this should be considered financial advice. What I share across all content mediums is a look at personal finance from my perspective. I cannot possibly know what is best for you, but I can share what I do in my own best interest.

Here’s a rundown of my life in August 2022, which will provide great context to my (somewhat outrageous) expenses.

I was wrapping up my two summer jobs in Victoria and preparing to head to France on a four-month study abroad trip. In between, I stopped in Kingston to visit friends and family before the pan-Atlantic flight.

In student fashion, I used my summer months to save, reduce my line of credit, and prepare for the upcoming school year. During this month I was able to earn a significant income, increase my emergency savings and pay myself first.

I now share with you August’s summary tables. You will notice this nomad-like month reflected in some specific classifications.

Check out the excel version by downloading below!

Classifying Debt and Taxes

Let’s look at my classification of debt and tax-related transactions.

I must begin by stating this general rule:

Both debt and tax-related classifications should be recognized in both the Income and Expenses summary tables. The reason is that, for both types of transactions, there is almost always some give and take. When I receive money I record it as an income, and when I pay back money (sometimes with interest) I record it as an expense.

Debt

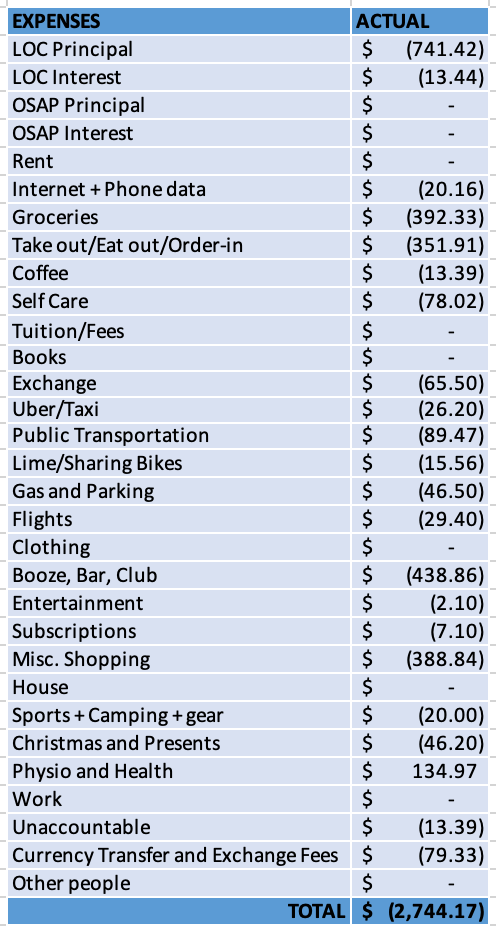

You’ll see on my tracker that any money received from my line of credit (LOC) or OSAP Loans (two sources of debt) is recorded in the income table, and any payments (that decrease my outstanding balance or pay interest charges) are recorded in the expense table. In August, I paid off $741.42 of my LOC principal plus an additional $13.44 interest charge, which are recorded under two separate classifications.

Remember: cash inflows (income) are positive numbers, and cash outflows (savings and expenses) are negative.

Oh, there's one more mention of interest.

The Credit Statement Table tells the story of your credit card over your credit period. Notice that interest is $0.00! If I were paying interest on my credit card I would include an interest classification in the expenses table.

Taxes

As for taxes, there are two ways you can go about recording these transactions.

Record all employment income as income BEFORE taxes (or “gross income”), then record tax payments and other deductions as an expense.

Record income after taxes (or “net income” - the amount that gets deposited into your account), and ignore the tracking of taxes.

I prefer the first method, for two reasons. First, you get to see firsthand how much is being taken off your paycheque. Second, following the true “Pay Yourself First” principle, you should pay yourself FIRST (meaning before the government) which means saving a desired percentage of your gross income.

Of course, you can see that I chose the lazy (net income) method. Why? Brace yourself - tax talk ahead.

When your employer takes taxes and other deductions off your paycheque, they are taking an estimate of what you would owe given employment at your wage/salary for the year. If you work for a full year, great - the tax withdrawals should be pretty close to your legitimate owing balance. In my case, I only worked for four months, but since my employer's estimates were based on a full year of employment they withheld more money from my pay than I would end up owing in taxes. At tax time, this over-withheld amount will be considered in the calculation of my tax refund.

Takeaway

File your taxes. The government isn’t going to come find you when they owe you money!

For the reason that I have historically received (and am likely to recieve) a tax refund for this over-payment, I put the Taxes and Gov Payments classification in the Income table. Plus, I am eligible for other government payments throughout the year that I recieve on a monthly basis (such as the $63.70 shown).

It is unlikely that I will recieve a tax refund after I graduate, so in 2023 I will be recording my taxes using the first method.

“Fun” Spending

Now that the boring stuff is over, let’s look at my “fun” spending - specifically the classifications Booze/Bar/Club and Take out/Eat out/Order-in.

Frankly, I am embarrassed at the totals I have racked up for these expenses - but I will use them as an exploratory moment (for you and for myself).

Quick Math

$351.91 on Take out/Eat out/Order-in

+ $438.86 on Booze/Bar/Club

= $790.78 on “fun” spending

… and this doesn’t even include groceries ($392.33), rent (lucky $0 for the summer), and miscellaneous shopping ($388.84 - more on this next substack).

Anyone who knows me knows that this is out of character. What happened?

A crazy August of saying my goodbyes in Victoria, visiting friends and family in Kingston, and meeting new friends in France racked up almost $800 on social drinking and eating. At the time, I knew I was overspending on these items, but keeping a keen eye on my finances up to this point gave me a deep understanding of my situation and what I could/couldn’t afford at the exact moments that I made these spending decisions.

In reality, who's to say whether $800 is too much? It’s too much for my liking given my other relatively high expenses, my (hazardously) low annual income, and my reliance on low-interest student debt. But we all lead different lives, so you do you!

My clarity about these expenses demonstrates how when life gets busy, you may spend wildly too. I bet you'd be surprised to know how much you spent on similar expenses in your busiest months. Start tracking and you can observe (and author) your own story.

To Be Continued…

Next Substack, we will continue with my August tracker and take a more rapid-fire look at some of my other classifications, such as Investments (PYF), Exchange Travels, and Miscellaneous Shopping. Plus, I will highlight the classifications that you will find handiest!

With that, I will wrap it up with an honourable mention of one of my favourite Substacks - Personal Financial Economics. Specifically, Mr. Puelz’s recent piece titled Description of Your Financial Life includes an “expense tracker” that you can access directly by following this link and downloading the file titled "Spending". Financial tracking is everywhere, people!!

Until next time. 👋